Blog

Complete guide to online payment methods for your business

Explore top online payment methods for businesses in 2026. Compare PayPal, Stripe, Apple Pay, and more to boost sales and customer satisfaction.

Expanding the ways that customers can pay you can be a shortcut to boosting sales, improving customer experience and streamlining your operations.

The world of “Visa or Mastercard?” is loooong gone and today’s consumers expect the businesses they support to keep up with a growing list of electronic payment methods.

Understanding the various types of payments available and how to accept online payments effectively is crucial for modern businesses.

But these increased options can benefit you as a seller, too. Competitors offer different terms, conditions, rates and features that you can select to align with your own needs and preferences and help you succeed in business. By accepting online payments through various forms of payment, you can also cater to a wider range of customer preferences.

When you know which platforms deliver what you need and are popular among your customer base, you’ve found the sweet spot that makes everyone happy. This guide will help you navigate the world of payment solutions and find the best payment methods for your business.

This guide reflects our research and perspective. Pricing and availability are current as of October 21, 2025. See something off? Tell us at hello@easy.tools.

Payment methods comparison

Key metrics explained

Setup difficulty:

- Easy: Sign up online, start accepting payments within hours

- Medium: Requires some configuration, business verification

- Complex: Technical integration, regulatory compliance, specialized knowledge

Technical expertise:

- None: Pre-built solutions, no coding required

- Basic: Simple integration, copy-paste code snippets

- Advanced: Custom API integration, developer resources needed

Settlement time:

- How long until funds are available in your account

- “Instant” means customer payment is processed immediately; merchant payout may vary

Decision guide for choosing the methods of payment

Step 1: Identify your business type

Are you primarily:

- Online-only e-commerce

- Physical retail with optional online presence

- Service provider (freelancer, consultant, agency)

- SaaS or subscription business

- B2B company

- Marketplace or platform

Step 2: Consider your average transaction size

Most of your transactions are:

- Under $50: Prioritize low fixed fees → Square, mobile payment apps

- $50-$500: Balance of percentage and fixed fees → PayPal, Stripe, cards

- $500-$5,000: Consider BNPL options → Klarna, Affirm, Afterpay

- Over $5,000: Optimize for lower percentage fees → ACH, GoCardless, RTP

Step 3: Assess your customer demographics

Your customers are mostly:

- Tech-savvy millennials/Gen Z: Add Apple Pay, Google Pay, Venmo, BNPL as preferred payment methods

- General consumers: PayPal, cards, Amazon Pay for secure payment methods

- Business professionals: ACH, wire transfers, traditional cards for B2B payments

- International: Stripe, PayPal, local payment methods (bank redirects)

- Apple users: Apple Pay is essential for mobile payments

- Android users: Google Pay is essential for mobile wallet options

Step 4: Match your geographic focus

You primarily serve:

- US customers: All major options available for accepting online payments

- European customers: Add bank redirects (iDEAL, Sofort), prioritize SEPA for preferred payment methods

- Global customers: Stripe, PayPal

- Specific regions: Research local preferences (WeChat Pay for China, PIX for Brazil, BLIK for Poland)

Step 5: Select your core payment stack

Recommended minimum:

- Credit/Debit cards (essential baseline for credit card payments)

- PayPal OR Stripe (trusted online payment gateway)

- Apple Pay + Google Pay (mobile/digital wallet for electronic payment methods)

Then add specialized options based on your answers above.

Detailed payment method profiles

PayPal

Setup difficulty: Easy | Technical expertise required: None | Processing speed: 1-3 days

Overview: PayPal is among the most popular payment methods and a globally recognized & trusted way to accept card payments online.

Key features

- Global reach: Used and accepted in over 200 countries

- Buyer and seller protection: Offers programs to protect both merchants and customers from fraudulent transactions

- Multiple payment options: Customers can pay with their PayPal balance, linked bank account or a credit/debit card

- Invoicing: Business accounts allow you to create and send professional invoices

- Integration: Integrates with popular e-commerce platforms like Shopify, Wix, and WooCommerce

Pros & cons

Pros: High level of customer trust, easy to set up, offers various forms of payment, including Venmo and “Buy Now, Pay Later.”

Cons: Fees can be higher than some competitors, especially for international transactions and funds can sometimes be held for security reviews.

Pricing structure

Get the latest updates on PayPal’s pricing policies here.

- Standard rate: 2.59-3.49% + $0.49

- Online credit and debit card payments: 2.99% + $0.49 per transaction

- In-person card payments (via Zettle): 2.29% + $0.09 per transaction

- Digital payments (PayPal, Venmo): 3.49% + $0.49 per transaction

- Volume discounts: Available for higher transaction volumes

- Monthly fees: None for standard accounts

- International fees: Additional percentage for cross-border transactions

Best use case

Ideal for small to medium-sized businesses and freelancers who need a simple, reliable and globally accepted payment solution without extensive developer-level customization.

Stripe

Setup difficulty: Easy to medium | Technical expertise required: Basic to advanced | Processing speed: 1-3 days

Overview: Stripe is a developer-focused payment processing platform known for its powerful APIs and highly customizable payment solutions.

Key features

- Developer-friendly APIs: Provides extensive documentation and a robust API for full customization of the checkout experience

- Subscription and billing management: Offers powerful tools for handling recurring payments and subscription payments

- Global payments: Supports over 135 currencies and a wide range of international payment methods

- Fraud detection: Includes built-in machine learning fraud detection tools to prevent payment fraud

Pros & cons

Pros: Highly flexible and scalable, excellent for businesses that want a custom-branded checkout, and supports a vast array of electronic payment methods.

Cons: Can be complex for non-technical users, and its advanced features may be overwhelming for very small businesses.

Pricing structure

Get the latest updates on Stripe’s pricing policies here.

- Standard rate: 2.9% + $0.30

- Standard online credit and debit card payments: 2.9% + $0.30 per transaction

- In-person payments: 2.7% + $0.05 per transaction

- Volume discounts: Custom pricing available for high-volume businesses

- Monthly fees: None for standard accounts

- International fees: Additional 1.5% for international cards

Best use case

Best for e-commerce businesses, online marketplaces and software platforms that require deep integration and a high degree of control over the payment process.

{{cta-banner-1}}

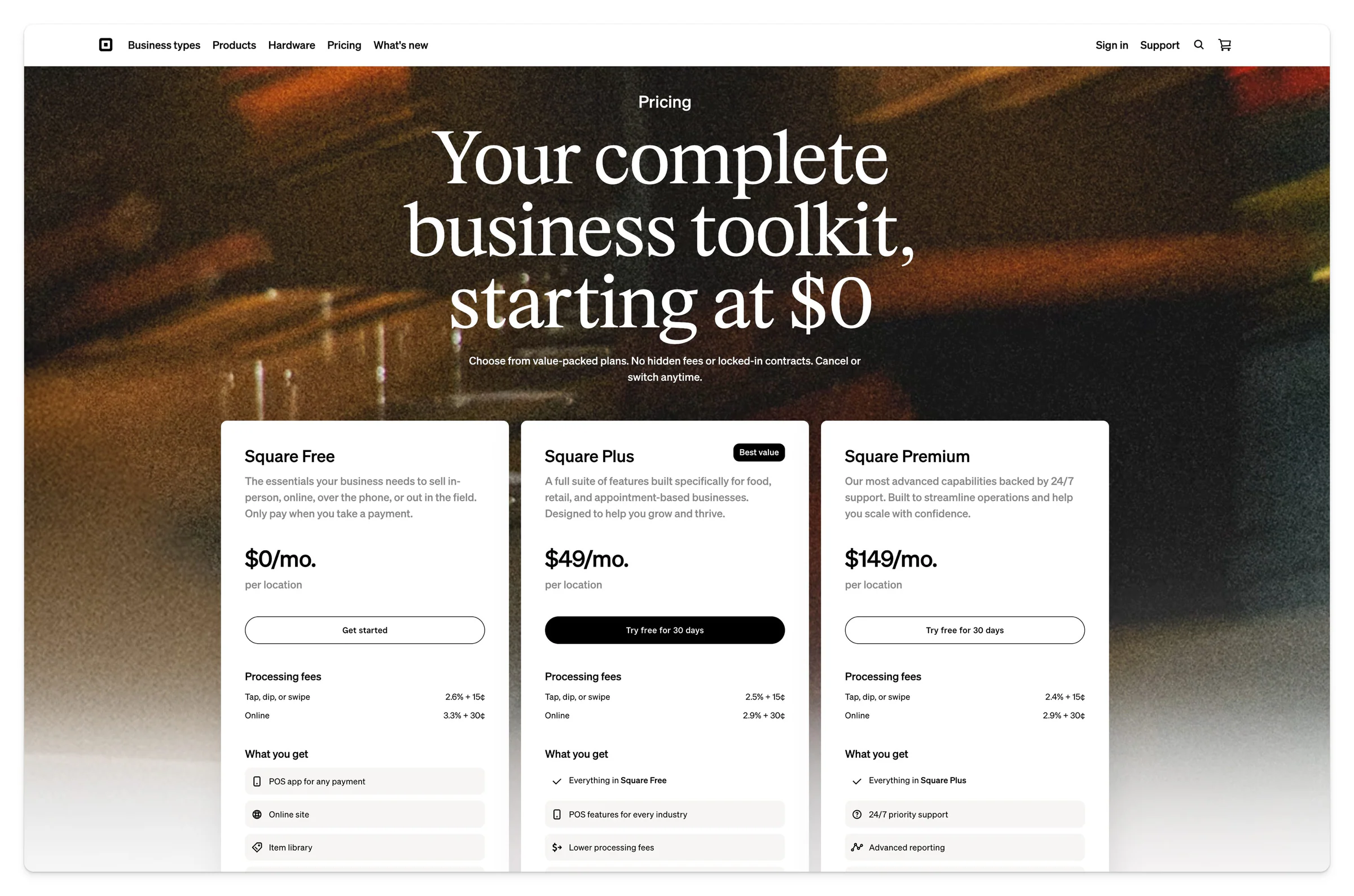

Square

Setup difficulty: Easy | Technical expertise required: None | Processing speed: 1-2 days

Overview: Square is a versatile payment solution, particularly popular for in-person sales with a comprehensive suite of POS (Point of Sale) tools.

Key features

- POS system: Offers free POS software and affordable hardware for in-person payments

- Omnichannel support: Seamlessly connects online stores, in-person sales, invoicing, and virtual terminals

- Free online store: Allows you to create and host a simple e-commerce website for free

- Business tools: Provides a full-service business ecosystem including payroll, marketing, and loyalty programs

Pros & cons

Pros: Affordable and easy to get started with no monthly fees for basic services, offers a free card reader for new merchants, and has a wide range of business management tools.

Cons: Fees for online and keyed-in transactions can be higher than card-present payments, and its POS functionality may not be as specialized as some industry-specific competitors.

Pricing structure

Get the latest updates on Square’s pricing here.

- Standard rate: 2.6-3.5% + $0.10-0.30 (depending on method)

- Online payments: 2.9% + $0.30 per transaction

- In-person swipe/chip: 2.6% + $0.15 per transaction

- Keyed-in transactions: 3.5% + $0.15 per transaction

- Volume discounts: Available through custom pricing

- Monthly fees: None for basic services; paid subscriptions for advanced features start at around $29/month

- International fees: Standard rates apply

Best use case

An excellent choice for small businesses, retail stores, food and beverage establishments and mobile merchants who need a simple and integrated system for both in-person and online sales.

GoCardless

Setup difficulty: Medium | Technical expertise required: Basic | Processing speed: 3-5 days

Overview: GoCardless specializes in bank-to-bank payments, particularly for recurring payments and invoices.

Key features

- Direct debit payments: Focuses on collecting payments directly from a customer’s bank account

- Recurring billing: Ideal for subscriptions, memberships, and installment payments

- Open banking payments: Utilizes open banking for fast and secure one-off payments

- Automated admin: Reduces manual work by automating payment collection and reconciliation

Pros & cons

Pros: Lower transaction fees compared to card payments, high success rate for recurring payments, and significantly reduces payment failure from expired or canceled cards.

Cons: Slower payment processing times compared to instant card payments, and primarily suited for businesses with recurring or one-off large payments, not impulse purchases.

Pricing structure

Get the latest updates on GoCardless’ pricing here.

- Standard rate: ~1% (with cap)

- Transaction fees: Generally lower than card payments, often a percentage of the transaction value with a capped maximum fee (e.g., 1% with a cap of a few dollars)

- Volume discounts: Available for higher transaction volumes

- Monthly fees: Varies by plan

- International fees: Depends on payment scheme (SEPA, BACS, ACH, etc.)

Best use case

Perfect for businesses with a subscription model, service providers (e.g., gyms, software-as-a-service) and any company that relies on predictable, recurring revenue.

Apple Pay

Setup Difficulty: Easy | Technical expertise required: None | Processing speed: Instant (funds settle per processor terms)

Overview: Apple Pay is a mobile payment and digital wallet service that allows users to make secure, contactless payments using their Apple devices.

Key features

- Enhanced security: Uses a device-specific number and a unique transaction code, so a customer’s card number is never stored on the device or shared with the merchant

- Seamless integration: Works with credit and debit cards stored in the Wallet app on iPhones, Apple Watches, iPads, and Macs

- Contactless payments: Enables tap-to-pay at physical terminals and a fast checkout experience online and in apps

Pros & cons

Pros: Extremely secure and private, fast and convenient for users, and integrates easily into the Apple ecosystem.

Cons: Limited to Apple device users, and merchants still pay the standard credit card processing fees to their payment processor.

Pricing structure

Get the latest updates on Apple Pay’s pricing here.

- Standard rate: Your payment processor’s standard rate

- Apple does not charge merchants or customers additional fees for using Apple Pay

- Businesses only pay their standard credit card processing fees to their payment processor

- Volume discounts: Through your payment processor

- Monthly fees: None from Apple

- International fees: Through your payment processor

Best use case

An essential payment option for any business with a physical presence (retail, restaurants) or an e-commerce store, especially those targeting tech-savvy customers who value security and convenience.

Google Pay

Setup Difficulty: Easy | Technical expertise required: None | Processing speed: Instant (funds settle per processor terms)

Overview: Similar to Apple Pay, Google Pay is a digital wallet and online payment system that allows users to make payments on various devices.

Key features

- Cross-platform: Available on Android, iOS, and web browsers, reaching a broad user base

- Tokenization: Creates a secure, virtual card number for each transaction, protecting the customer’s actual card information

- Loyalty and offers: Can store loyalty cards, gift cards, and coupons, offering a streamlined experience for customers

Pros & cons

Pros: Wide acceptance across platforms and devices, secure, and offers a fast checkout experience.

Cons: Like Apple Pay, merchants are still subject to their standard payment processing fees.

Pricing structure

Get the latest updates on Google Pay’s pricing here.

- Standard rate: Your payment processor’s standard rate

- Google does not charge extra fees to merchants for accepting Google Pay

- Merchants pay the standard transaction fees to their payment processor

- Volume discounts: Through your payment processor

- Monthly fees: None from Google

- International fees: Through your payment processor

Best use case

A must-have for any business looking to cater to a large user base on Android and other platforms, particularly in e-commerce and mobile apps.

Amazon Pay

Setup difficulty: Easy | Technical expertise required: None | Processing speed: 1-3 days

Overview: Amazon Pay allows customers to use their Amazon account information to make purchases on external websites and apps.

Key features

- Customer trust: Leverages the trust and familiarity customers have with the Amazon brand

- Simplified checkout: Customers can skip creating a new account and instead use their existing Amazon login and stored payment information

- Fraud protection: Backed by Amazon’s fraud detection technology

Pros & cons

Pros: Increases conversion rates by simplifying the checkout process, particularly for customers who are reluctant to create new accounts or enter their card details.

Cons: Not as widely available on all shopping platforms, and may offer fewer rewards or cashback compared to other payment methods.

Pricing structure

Get the latest updates on Amazon Pay’s pricing here.

- Standard rate: ~2.9% + $0.30

- Businesses pay a processing fee per transaction, similar to other card payments

- Volume discounts: Available for qualifying merchants

- Monthly fees: None

- International fees: Varies by region

Best use case

Ideal for e-commerce businesses that want to reduce cart abandonment and tap into the vast network of Amazon customers.

ACH Transfers

Setup difficulty: Medium | Technical expertise required: Basic | Processing speed: 1-3 days

Overview: Automated Clearing House (ACH) transfers are electronic, bank-to-bank payments processed through the ACH network.

Key features

- Cost-effective: Generally have much lower fees than credit card transactions

- Reliable: Secure and regulated by NACHA (National Automated Clearing House Association)

- Automation: Perfect for recurring payments, direct deposit payroll, and vendor payments

Pros & cons

Pros: Very low cost, highly secure, and great for automating regular payments.

Cons: Slower than card payments, typically taking 1-3 business days to settle, and can have transaction limits.

Pricing structure

Get the latest updates on ACH Transfers pricing through your payment processor.

- Standard rate: $0.20-1.50 flat fee per transaction

- Fees are typically low, often a flat fee per transaction

- Makes ACH very cost-effective for large transactions

- Volume discounts: Often available

- Monthly fees: Varies by provider

- International fees: ACH is US-only; international requires wire transfer or alternative

Best use case

Best for B2B transactions, payroll, rent payments and any business that handles large, recurring payments where speed is not the primary concern.

Credit and debit cards

Setup difficulty: Easy | Technical expertise required: None | Processing speed: 1-3 days

Overview: Credit and debit card payments are the most common and universally accepted form of electronic payment methods.

Key features

- Universal acceptance: Accepted almost everywhere, both online and in person

- Flexibility: Debit cards draw directly from a bank account, while credit cards offer a line of credit

- Fraud protection: Credit cards, in particular, offer strong fraud protection and chargeback rights

- Rewards: Many credit cards offer rewards, cashback or points, which incentivize their use

Pros & cons

Pros: High convenience, universally understood and trusted by consumers.

Cons: Higher processing fees for merchants, and a risk of chargebacks and fraud.

Pricing structure

For the latest updates on credit card fees and pricing, visit the website of your payment processor.

- Standard rate: 2.5-3.5% + $0.15-0.30

- Merchants pay interchange fees, assessment fees, and processor markups

- Typically a percentage of the transaction plus a small fixed fee (e.g., 2.9% + $0.30)

- Volume discounts: Available for high-volume merchants

- Monthly fees: Varies by processor

- International fees: Additional 1-3% for foreign cards

Best use case

Essential for any business. Accepting credit and debit card payments is a baseline expectation for customers. No business, online or off, can succeed without this way to receive payments.

Buy Now, Pay Later (BNPL)

Setup difficulty: Easy | Technical expertise required: None | Processing speed: Instant for merchant payout

Overview: BNPL has quickly become a common online payment method, allowing customers to split a purchase into smaller, interest-free installments. Popular platforms include Klarna, Afterpay, and Affirm.

Key features

- Installment payments: Breaks a large purchase into manageable, interest-free payments

- Increased conversion and AOV: Reduces “sticker shock,” leading to higher conversion rates and a larger average order value (AOV)

- Immediate payout for merchants: The BNPL provider pays the merchant the full amount upfront, assuming the risk of non-payment from the customer

Pros & cons

Pros: Drives sales, reduces cart abandonment and attracts new customers, especially younger demographics.

Cons: Merchants pay a higher fee per transaction than standard card payments and it can introduce fraud risks.

Pricing structure

BNPL fees vary by provider (Klarna, Afterpay, Affirm, etc.).

- Standard rate: 4-6% + fixed fee per transaction

- Fees are typically higher than credit card fees

- Often range from 4-6% plus a fixed fee per transaction

- Volume discounts: Sometimes available

- Monthly fees: None

- International fees: Varies by provider and region

Best use case

Great for businesses selling higher-ticket items like electronics, furniture or apparel, as it makes these purchases more accessible to a wider range of customers.

Cryptocurrency payments

Setup difficulty: Complex | Technical expertise required: Advanced | Processing speed: Minutes to hours

Overview: Cryptocurrency payments involve transactions using digital currencies like Bitcoin, Ethereum, or stablecoins.

Key features

- Decentralized: Not controlled by a central authority like a bank or government

- Fast transactions: Can offer faster transaction times than traditional banking methods

- Lower fees: Can have lower transaction fees, especially for international payments

Pros & cons

Pros: Can attract a new customer base, offers lower fees, and provides a level of anonymity and security.

Cons: Highly volatile value, still a niche payment method with limited mainstream adoption, and can be complex to integrate and manage.

Pricing structure

Fees vary by cryptocurrency and payment processor.

- Standard rate: Variable, typically 0.5-2%

- Fees can be very low, but can also fluctuate based on network congestion

- Payment processors that handle crypto for you will have their own pricing models

- Volume discounts: Varies by processor

- Monthly fees: Varies by processor

- International fees: Generally none (inherently borderless)

Best use case

Best for tech-forward businesses or those with a global customer base that are looking to cater to a specific, cryptocurrency-savvy audience.

Mobile payment apps (Venmo, Cash App)

Setup difficulty: Easy | Technical expertise required: None | Processing speed: Instant to 1 day

Overview: Mobile payment apps like Venmo and Cash App are primarily used for peer-to-peer (P2P) transfers, but they also offer business payment options.

Key features

- P2P and business payments: Allows users to send and receive money from friends and also pay businesses

- Social integration: Venmo, in particular, has a social feed that allows users to share transactions, creating a social element

- Instant transfers: Offers fast fund transfers between users

Pros & cons

Pros: Taps into a large, established user base and can be a convenient way for customers to pay.

Cons: Primarily used for P2P, so it may not be seen as a professional payment option for all business types.

Pricing structure

Pricing varies by platform.

- Standard rate: 1.9-2.9% + $0.10

- Business transactions typically incur a small percentage fee (e.g., 1.9% + $0.10 for Venmo for business)

- Volume discounts: Rare

- Monthly fees: None

- International fees: Limited or no international support

Best use case

Great for small businesses, freelancers and service providers who deal with a younger, tech-savvy clientele, particularly for in-person transactions or small-ticket services.

Prepaid cards

Setup difficulty: Easy | Technical expertise required: None | Processing speed: 1-3 days

Overview: Prepaid cards are loaded with a specific amount of money and can be used for purchases like a debit card.

Key features

- No credit check: Accessible to individuals with limited or no credit history

- Budgeting tool: Helps users manage their spending by limiting the amount available

- Wide acceptance: Accepted wherever the card network (e.g., Visa, Mastercard) is accepted

Pros & cons

Pros: Simple to use, and offers a level of spending control.

Cons: Often comes with various fees (activation, reload, inactivity), and does not build a credit history.

Pricing structure

Terms are typically the same as those used for branded “Visa” and “Mastercard” credit cards.

- Standard rate: Your processor’s standard card rate

- Merchants pay the same fees as a standard credit or debit card transaction

- Volume discounts: Through your payment processor

- Monthly fees: None from prepaid card perspective

- International fees: Through your payment processor

Best use case

Not a primary payment method for businesses, but it’s important to recognize that customers may use them for purchases and they are processed like any other card.

Bank redirects (e.g., iDEAL, Sofort)

Setup difficulty: Medium | Technical expertise required: Basic | Processing speed: Instant confirmation, 1-3 days settlement

Overview: Bank redirects are a type of payment method common in Europe that allows customers to make payments directly from their bank account using their online banking portal.

Key features

- Direct bank transfer: The payment is authorized and processed through the customer’s bank

- High security: Relies on the bank’s secure login and authentication process

- Instant confirmation: The merchant receives immediate payment confirmation

Pros & cons

Pros: Highly secure, trusted by consumers in the regions where they are used, and often have lower fees than card payments.

Cons: Geographically limited (e.g., iDEAL is dominant in the Netherlands, Sofort in Germany and Austria), and the process can sometimes feel complex compared to a one-click checkout.

Pricing structure

Fees depend on the specific bank redirect method and region.

- Standard rate: Low percentage or flat fee (typically 0.5-1.5%)

- Fees are generally lower than credit card transactions

- Often a flat fee or a very low percentage

- Volume discounts: Available through some providers

- Monthly fees: Varies by provider

- International fees: Designed for specific regions

Best use case

Crucial for businesses operating in regions where these payment methods are culturally preferred, as it’s often the default online payment option for many consumers.

Real-Time Payments (RTP)

Setup difficulty: Medium | Technical expertise required: Basic to advanced | Processing speed: Seconds

Overview: Real-time payments are a new wave of electronic payment methods that allow funds to be transferred and settled almost instantly, 24/7.

Key features

- Instant settlement: Funds are available in the recipient’s account within seconds

- 24/7/365 availability: Payments can be made and received at any time

- Irrevocable: Once a payment is authorized, it cannot be reversed

- Rich data: Payments can be sent with more data, making reconciliation easier

Pros & cons

Pros: Improves cash flow, enhances customer experience and streamlines back-office operations.

Cons: New types of fraud, such as authorized push payment (APP) fraud, are on the rise, and widespread adoption is still a work in progress in many regions.

Pricing structure

Pricing varies significantly by provider and region.

- Standard rate: Variable (often lower than wire transfers)

- Pricing can vary, but generally aims to provide a low-cost alternative to traditional wire transfers

- Volume discounts: Often available

- Monthly fees: Varies by provider

- International fees: Limited international availability currently

Best use case

Excellent for B2B payments, on-demand services, gig economy payments, and any situation where immediate access to funds is critical.

Common payment method combinations

Different business models benefit from specific payment method combinations. Here are proven stacks for various scenarios:

Small online business starter stack

Core foundation for e-commerce beginners:

- Credit/Debit Cards (essential)

- Stripe or PayPal (trust and global reach)

- Apple Pay + Google Pay (mobile shoppers)

Why this works: Removes price barriers through installments, builds trust with buyer protection, appeals to different financial preferences.

Mobile-first business stack

For app-based businesses and mobile commerce:

- Stripe (mobile SDK)

- Apple Pay (iOS users)

- Google Pay (Android users)

- In-app purchase options (for digital goods)

Why this works: Optimized for mobile checkout speed, leverages device security features, minimal friction for mobile users.

Marketplace platform stack

For platforms connecting buyers and sellers**:**

- Stripe Connect (split payments)

- PayPal (seller payouts)

- Credit/Debit Cards (buyer payments)

- ACH Transfers (seller withdraw

How to accept payments online - Final recommendations

Like so many other aspects of the digital marketplace, the world of online payments is constantly evolving and the best strategy is to offer a mix of options that cater to your specific business and customer base.

Your action plan

Phase 1: Essential Foundation (Week 1)

- Set up credit/debit card processing

- Add PayPal or Stripe

- Integrate Apple Pay and Google Pay

Phase 2: Strategic expansion (Month 1-2)

- Analyze your customer demographics and transaction data

- Add 1-2 specialized payment methods based on your business model

- Test conversion rates and customer feedback

Phase 3: Optimization (Month 3+)

- Review transaction costs and settlement times

- Negotiate better rates with high-volume processors

- Add region-specific or niche payment methods as needed

- Monitor industry trends and emerging payment technologies

Payment methods - Key takeaways

- Credit and debit cards remain non-negotiable - this is your baseline

- Digital wallets (Apple Pay, Google Pay) are now standard - customers expect them

- Match payment methods to your business model - subscriptions need different tools than retail

- Consider your customer demographics - younger audiences expect BNPL and mobile options

- International businesses need localized payment options - one size doesn’t fit all markets

- Balance convenience with cost - more options help sales, but fees add up

- Test and measure - track which payment methods drive conversions

- Stay current - payment technology evolves rapidly

The exact mix that works best for a particular business will depend on matching needs to the features, pros, cons and pricing of each method. Still, the lesson that applies equally to all is that a flexible, customized payment ecosystem is a must-have for any successful retailer.

Start with the essentials, then expand strategically based on your unique business needs and customer preferences.